|

|

|

|

|

Werner International now registered with the IMC

Werner International is pleased to

announce to all of our Egyptian clients that we are now registered with the IMC

(Industries Modernization Center) as a training provider.

Being approved by the IMC represents significant benefits to the local

companies.

The excellent capabilities of Werner International in the development of the

labour force and management sectors are well known worldwide. The company offers

training programs for the various industrial sectors as well as supervision and

management development courses.

The training programs are highly customizable and cover the entire technical

spectrum from spinning to garment making, quality management, styling, and

design, merchandising and marketing.

Companies interested in receiving more information about these exciting new

development tools should contact Saskia Dornez in our Brussels office at

info@wernertex.com.

Back to top

|

|

|

The Werner International PARTNER SEARCH SERVICE

As the world continues to change

at a rapid pace, the textile and fashion industries are changing even more

rapidly. While new economies emerge, new ways of consumption are taking place,

new production patterns are being designed and new supply chains are then

required. �Speed� is becoming a key word, where �quick service�, �fast fashion�,

�fast retailers� are the winning concepts.

As more and more retailers and fashion brands are leading the market, the supply

chains are getting more complicated every day. It is not unusual to see a

finished garment whose yarn is spun in India or China; the fabric is woven in

Turkey or Egypt; finished in Italy; and then made-up in Romania. Such a

complicated production and supply pattern requires a network of partners, rather

than simple suppliers. The key players � the retailers and the fashion brands �

become mere �orchestrators� of a complex network, where each link is at time a

supplier or a customer.

Furthermore, strategic alliances become the key to allow for small-medium sized

enterprises to rapidly grow - or sometimes to just survive. Being part of a

complex system may be the only way to get out of �isolation� and take advantage

of all the opportunities offered by global markets. Industrial or commercial

(equity or non-equity) joint-ventures, mergers and/or acquisitions can offer a

number of advantages in terms of increased competitiveness, efficiency, market

share acquisition; all in a relatively short time frame.

A correct quality/price ratio and the best service (in terms of quick deliveries

or �customization�) are the key success factors in today�s textile and apparel

industry. This can only be offered if the whole supply chain is made up of a

number of reliable partners: the key phrase nowadays is �look for the right

partner�, rather then �look for the cheapest supplier.� It is important to find

the right partner who will be able to serve the best quality at the right price

in the shortest time.

This is exactly why Werner, through its network of offices, representatives,

�antennas� and industry contacts located at every level, has been able to

successfully establish its PARTNER SEARCH SERVICE.

Starting a few years back, the number of requests for a partner search have been

increasing on a daily basis. Textile and apparel companies benefit from Werner�s

support when they need to find a buyer or investor, look for a company or brand

to purchase, or locate an industrial partner to associate with in a

joint-venture company. The number of companies we have contacts with, and the

number of countries in which we operate in, are so wide that we can virtually

�match� partners from every corner of the world.

The search is based on a first preliminary assessment. At this point we analyse

the exact requirements, capabilities, competences and strengths of the

applicant; then we profile the ideal future partner on the basis of our thorough

understanding of these markets. Next, the actual search will be conducted

through local contacts and direct interviews with the potential targets, along

with the advice of industry leaders. The objective of the service is not only to

introduce parties, but also to assist in understanding the level of a strategic

match and assist our client in the negotiation process. A deem of absolute

confidentiality is taken all throughout the process - guaranteeing that no

sensitive information whatsoever will be disclosed. The actual search is

conducted in the most confidential way, bearing in mind how the news could cause

harmful rumours to spread throughout the entire industry segment.

If your company is looking to become a key player in a successful new global

supply chain and is looking to explore new strategic partnership opportunities,

please e-mail Werner at info@wernertex.com. We will respond back to you

immediately to organize an initial appointment and assessment of the project.

Back to top

|

|

|

|

|

(click to enlarge) |

|

|

|

|

|

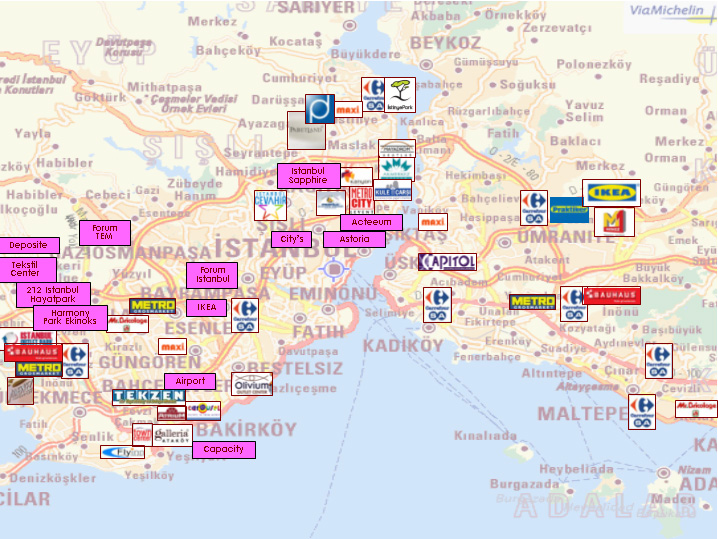

Shopping Centers in Turkey

After the year 1980, while under

the leadership of Prime Minister, Turgut Ozal, Turkey went through a phase of

neo-liberal politics and liberalization of foreign direct investment. During

this period, the level of imports increased and privatization projects were

initiated. With such an outlook, in 1988 Turgut Ozal initiated the construction

of the first shopping mall, located in Istanbul, named the Galleria Shopping

Center. Since this was the first shopping mall, the scope of it was not only

limited to just close proximity to Bakirkoy and Atakoy, but rather throughout

all Istanbul. There were even people visiting Galleria from many other Turkish

cities.

In the 1980s Turkey had the sum total of only 3 malls. After the opening of

Galleria, others began to open in Ankara, Izmir, Adana, Bursa and other cities.

In the 1990s this number increased to 35, with the opening of several new malls.

To name a few: Akmerkez (1993), Capitol (1993), Carousel (1995), CarrefourSa,

(1996), Grandhouse (1997), Migros (1998), Profilo (1998), Mayadrom (1998) in

Istanbul, and Atakule (1989), Karum (1991), Galleria (1995), Bilkent (Real and

Praktiker) (1997) in Ankara.

There is at least one shopping center in 32 of the city centers in Turkey.

Istanbul has the most locations with a total of 53, followed by 16 in Ankara and

12 in Izmir. According to the data presented in the �Retail Catalogue� by Social

Communication and Consultancy, the greatest boom was after the millennium. In

just the past 7 years, the number of shopping centers has increased to 149. In

2006 alone, 27 new shopping centers opened. In the first 3 quarters of 2007, 13

new centers opened, and 83 more centers are projected to be finished by the end

of 2007.

Gunduz Bayer, the General Manager of Metro Group Asset Management, has stated

that for every 1000 persons there is 32 sqm of shopping mall space in Turkey;

this figure is still very low when compared to Europe or the US. He added that

more than 100 of the shopping centers (including hypermarkets) in Turkey (more

than 200 in total) are in Istanbul, and therefore more are needed in Anatolia.

He expects that the number of shopping centers will increase to 500 in total

within the next five years, and the weight will be shifted towards Anatolia.

It is expected that within the next 10 years, the new tendency in bigger cities

will be to introduce outlet malls, specialized malls and entertainment centers.

For example, the Multi Turk mall company is planning to construct the country's

largest mall, Forum Istanbul, a 150,000 sqm complex with shops, leisure

facilities, offices, residential property and a hotel. Ankara, Izmir, Antalya

and Bursa are also attracting real estate investors. Multi Turk mall is planning

to build "Forum Etik" in the capital of Ankara, while in Izmir; the same

developers are working on the 66,000 sqm Forum Bornova.

With these developments, there are environmental and social risks to be taken

into consideration. Planning and infrastructure are very important. In Istanbul,

Istinye Park is the most recent shopping mall opened, combining many well-known

global brands such as Armani, Gucci, Louis Vuitton, Dolce & Gabbana, Coach,

Chlo�, Paul Smith, etc. It also includes well-known Turkish brands - all under

the same roof.

Certain questions always arise with the rapid development of shopping centers in

Turkey. An example, in Istanbul:

-

Is the infrastructure

sufficient, in terms of roads, transportation, electricity, water, etc?

-

Will enough traffic be

generated in the different shopping centers around the city?

-

Will the purchasing power of

the population be sufficient for these retail stores to survive?

There are different opinions

regarding the answers of these questions. Istanbul is a big city, with a

population of about 15 million people, with an intense traffic jam throughout

the day. Therefore, the vicinity of the shopping center becomes the number one

criteria to select a location to shop. The young population especially prefers

one-stop shopping centers where they can shop, eat, go to the movies, do grocery

shopping, use the dry cleaning service, etc.

However, as this industry is developing, the Turkish brands are opening stores

in all of the locations, regardless of their positioning. Therefore, in the

future they will have to be more selective in choosing new locations. The basic

reason cannot continue to be �because their competitors are there�.

Another question mark is the opening of global luxury brands in Turkey. The

small portion of the population, who can actually afford to buy these brands,

would mostly prefer to shop during their travels around Europe. Thus, resulting

in less spent in Turkey, because the prices are at least 20% higher than the

original prices, which is due to the high import taxes. For this reason, another

factor to be taken into consideration is that the tourists coming to Turkey will

also not be buying at the shopping centers.

In conclusion, this boom in the development of shopping centers will have great

effects on the economy, the purchasing behavior of the buyers, the lifestyles of

the consumers, and the establishment of brands in Turkey.

Back to top

|

|

|

|

|

(click to enlarge)

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Strategic Overview on Global Textile & Apparel Supply Chains Dynamics

WERNER INTERNATIONAL

-

Werner

is a management consulting practice globally active since 1939, focused

exclusively on assisting the textile, apparel and fashion industry in

improving its performance and optimising its activities.

-

Werner

is unique, combining specialised expertise in all technical areas of the

supply chain with global marketing know-how and exceptional networking.

-

Werner

operates throughout the world with an

international team of highly specialized senior

consultants and regional or national representatives coordinated through

three operational offices in Brussels, Washington and Beijing.

WERNER

SERVICES

TECHNICAL AREA

-

Benchmarking for all manufacturing activities

-

Productivity improvements & control

-

Product

Development management

-

Total

Quality management

-

Manufacturing standards and control

-

Preventive

maintenance

-

Standard

cost system design

-

Supervisor

& operator training program

-

Management

training and development

-

Sourcing

strategy and suppliers accreditation

-

Management

Information Systems

-

New plant

start-up

MARKETING

AND STRATEGY AREA

-

Market

intelligence and strategic market analysis

-

Audit e

benchmarking for the marketing, branding and retailing areas

-

Top

Management training

-

Partners

search

-

Acquisitions e Joint Ventures

-

Strategic

Business Planning

-

Development

of Global sourcing strategies

-

Marketing

Strategies

-

Merchandising management

-

Retail

management

-

Brand

development

SOME

CUSTOMERS

-

Over 65

years of consulting in textile/apparel/fashion industry

-

Over 5,000

assignments carried out

-

Presence in

more than 65 countries

Perspective

1:

A global industry mature for

growth outside traditional western markets

-

Since 2005,

the world textile and apparel industry has accelerated in its complex

transformation

-

A new world

of competitors (but also consumers) has entered the global market with their

impressive capabilities and will to growth

-

By 2010

China is expected to represent 40/45% of global trade, India 17/20%

-

Despite its

impressive growth trend, China's rising costs and perceived risks are

creating relevant opportunities for other low cost countries

-

India is

rapidly expanding its role with a heavy weave of new capacity build-up

invertical integration

-

Pakistan,

Vietnam, Cambodia and Bangladesh are leveraging on their low manufacturing

costs and building up more textile capacity

-

Egypt is

currently looking at textiles with new emphasis

-

Turkey is

becoming a critical regional player, closely connected to Italy,

repositioning and creating a number of new regional brand

players(Turquality)

-

Eastern

European countries, due to their growing costs are rapidly refocusing and

repositioning on higher market segments

-

South and

Central America maintain a relevant focus on textile

-

Italy still

defends its role in the luxury segments

Imports Penetration inWestern Markets

(click to enlarge)

Mature USA Apparel Market

(click to enlarge)

Mature EU Apparel Market

(click to enlarge)

-

While T&A

consumption in Western markets grows moderately, imports have almost reached

85-90%

of total consumption

-

We must now

face the impact of the

capacity bubble built

in anticipation of market opening and quota removal and creating a

deflationary environment

-

However,

the time gap between the positive and negative effects of liberalization is

too often driving us to forget about the

real mission

of trade liberalization

Per Capita Consumption

(click to enlarge)

WORLD TEXTILE & APPAREL TRADE

(click to enlarge)

NEW

MARKETS

The future global market for textile and apparel is expected to witness a

relevant expansion thanks to:

-

Consumption

growth in new markets

-

Global

expansion of Modern retail space

-

Eastern

Europe and ex Russian block

-

Turkey and

Middle East

-

South East

Asia

-

India

-

China

-

South

America

Retail Expansion Across

Europe

New retail surface 2006-2008 -INDEX

(click to enlarge)

Recap Global Industry

-

Commodities

Bubble

-

Hegemonic

role of India & Chinawith their integrated supply chains

-

Need for

differentiation to sustain premium producers (Italy . turkey)

-

Continuous

fight for commodity markets and cost leadership

-

Boom of

air/sea shipments

Perspective 2:

Newly shaped global supply and

value chains

Global Supply Chain Models

(click to enlarge)

Global Supply Chain Models

(click to enlarge)

Production Volume: Traditional VS Strategic

(click to enlarge)

Labour Cost Comparison

(click to enlarge)

Transformation of Value

Chains

Value adding today still means "better" products (value = differentiation) but

increasingly more

service-rich products

(value = service + intangibles)

-

Luxury

segments still heavily rely on the European textile supply chain for their

exclusivity and differentiation requirements

-

All other

market segments share quite similar "intrinsic" products differentiated by

their service content

Value is today

created less and less on intrinsic quality and increasingly on intangible

properties:

Perspective 3:

Strategic snapshots

-

Skills &

Competences

-

Key Trends

Strategic

Snapshots: Skills & Competences for Success

-

Orchestrators & Merchandisers

-

Brand

management

-

Innovation

-

Characterization and differentiation and of standards -Time to market

Strategic

Snapshots 1: Orchestrators and Merchandisers

Supply Chain Orchestrators

Capability to orchestrate fragmented and disperse textile supply chains

leveraging on intelligence, understanding, technology and organizational

practices

Merchandisers

Capability to create "consistency" across ranges developed and produced across

the globe - leveraging on clear range architecture

Strategic Snapshots 2: Retail and B2B Branding

Retail brands

Growing in importance to

create differentiation, loyalty and premiums

B2B branding

In a global world of

options, large retailers and brands are loosing product know-how and rely more

and more on B2B brands

Strategic Snapshots 3: Innovation

Innovation

The global market is eager

for innovation: new products, new integrated systems, new application...

Strategic Snapshots 4: Differentiation & Characterization

The global industry desperately needs fast and effective differentiation and

characterization of standard products:

-

adding value to standard products at the latest stage possible + New need for

"fast" and custom will soon boom with

internet

- Zara model changing the industry

Strategic Snapshots: Key Trends

-

No More

Seasons

-

External

factors torapidly change scenarios

-

Customization & the Web

Strategic Snapshots: No More

Seasons

Strategic Snapshots:

External Factors

-

Exchange

rates $, Euro, Yuan, Rupee...

-

Petrol and

direct impact of MMF & Air transport...

-

Political

situation...

...can change global landscapeand supply chains in a few months

Strategic Snapshots:

Customization & the Web

-

Internet

sales rapidly growing (US and north Europe)

-

Focus on

specific product categories

-

Will be a

relevant channel for apparel sales

-

Example:

www.NIKEiD.com

Final Message

It is going to be a challenging global market full of threats but also full of

incredible opportunities

It is going to be a talent intensive market where talent will be key success

factor

Thank You!

click here to download the pdf version of this article

Back to top

|

| |