|

A MESSAGE FROM THE PRESIDENT

Dear Colleagues,

As we enter the New Year it is worthwhile to look back and consider our keynote

for 2012, and at the same time to look forward to what 2013 is likely to bring.

The year 2012 will enter into history as a year of economic turmoil and weak

consumer spending, caused by the Eurozone crisis and its impact on a worsening

financial and economic performance. For entrepreneurs and workers in the textile

and clothing industries, globalization was self-evident. The global impact of

the Eurozone and financial crisis now made very clear that also the financial

industry is a global business, affecting every layer of the economic system,

particularly globalised industries and consumer markets like the textile &

clothing industries.

But every cloud has a silver lining and as we have experienced in the textile

industry for so long now, every crisis is bringing new opportunities. It was an

exciting year for Werner International, both on the technical and marketing

front. Werner International’s efficiency, quality and productivity programmes

were in high demand and our global marketing coverage has assisted many

companies in improving their supply chains and sales performance. We have seen

our presence grow substantially in several markets - including India, South-East

Asia, Argentina, Turkey and the USA.

In today’s global competitive environment, companies are looking for ways to

increase their market shares either through volume or value services, satisfying

the needs and demands of each segment and area of the market. Consumers are

getting more and more informed and conscious regarding their spending and styles

of life. Companies have the choice of reducing their manufacturing costs by

either increasing their efficiency and productivity, or through continued

re-location of their manufacturing bases. Important decisions are being made

every day by many companies around the world to choose alternative suppliers

according to the product characteristics, targeted quality levels and costs, and

service scope. These decisions are also supported by investments in Human

Resources, training of employees, and re-organization of existing structures. We

are also witnessing an era of consolidation of businesses, emphasis on

sustainable production and green manufacturing. Social and corporate

responsibilities remain important aspects for brands and retailers.

Included in this edition of the New Twist are several articles that I am sure

will be of high interest to you:

- The renowned Werner International Labor Cost Comparison 2012 edition

- Overview from the 38th National Textile Industry Symposium of Mexico, with

Werner International as key note speaker

- Sourcing from China and South East Asia: the Werner view

At the beginning of this New Year I wish to extend to you, your colleagues and

families, my very warm and sincere wishes for a year of happiness and

prosperity.

Sincerely,

Constantine Raptis

President – Werner International

~ ~ ~ ~ ~

We are excited to start off the New Year by attending the first tradeshows in

January 2013, including

- Pitti Uomo in Florence (8 to 11 January 2013)

- Bread & Butter in Berlin (16 to 18 January 2013)

To set up an appointment with one of our attending consultants, kindly contact

us at info@wernertex.com and we will

arrange a meeting.

Back to top

WERNER INTERNATIONAL @ THE 38th NATIONAL TEXTILE INDUSTRY SYMPOSIUM OF MEXICO

Werner International was at the 38th National Textile Industry Symposium of

Mexico, organized by Canaintex, with the attendance of leading industry experts,

government officers, representatives of institutions and associations related to

the industry.

The Symposium was organized by Canaintex, the organization supporting the

textiles and fashion industries in Mexico.

The 2-day Symposium brought out some interesting facts and created a fruitful

platform for discussion and possible industry solutions.

Some interesting points were:

Mr. Bruno Ferrari, the Secretary of Economy emphasized the topic of “innovation”

and that Mexico needs to produce in a different way, while also being

transparent and with a solid legal base.

The textile industry is an important one in Mexico as it generates a significant

portion of exports and creates a base for employment.

- Garment exports have increased by 8.4% last year

- Export of oil is approximately 16%

- A decline from 86% to 76% in the trade between Mexico and the USA

- 50% of the population is younger than 25 years old.

In 2012 :

- The GDP growth of Mexico was noted at approximately 4%

- The consumption growth was noted at 4% as well

- The installed capacity has increased by 6-10%

- The employment levels are noted as above the US levels

- Retail sales has increased by 4-6%

- Exports have increased by 10-15%

Among the discussions and speeches of various industry experts, it was also

agreed that the USA crisis had a very negative impact on the USA - Mexican trade

in the past four years and that the share of business with the USA has

decreased.

It is now time to act as a unity with the NAFTA countries and establish market

entry strategies as a unified group towards other markets.

Among this global environment, China is a big influencer with cost competition.

It has already gained a market share worth 4 billion USD, taken from the share

of Mexico in trade figures towards the USA.

However, with the ever changing global environment, some of the cost advantages

of China are also starting to fade away, due to the increase in exchange rates,

increase in labor costs, increase in oil prices, and thus transportation costs,

etc. Therefore, the USA market has started looking for proximity suppliers

(“closer-to-home” solutions) to balance the cost of production, which would in

return positively reflect on the share of Mexican exports into the USA market.

Another important international development will be depending on the

Trans-Pacific Partnership agreement between the countries of Canada, USA,

Mexico, Peru, Chile, Vietnam, Malaysia, Singapore, Brunei, Australia and New

Zealand. As a result of this agreement, this group of countries will be having a

free trade agreement among each other and it will surely change the “rules of

the game” for the sourcing activities and supply chain organizations of major

retailers and brands around the world.

It has been pointed out how the Mexican industry as a whole, developing as a

"commission maker", has never been able or interested or lead to create a truly

Mexican brand. As It is a clear fact that Mexico cannot compete solely on price

anymore in the textile industry, it has now become evident the need to invest in

the manufacturing and creation of value-added products, as well as

technologically enhanced product segments to re-position - in order to survive

in the highly competitive global textiles and fashion industries. Hence a new

project has been presented, that will be implemented in the next few months,

aimed at the establishment of Innovation Centers to support the development of

the innovation, design and branding capabilities of the textile and fashion

industry.

Back to top

2011 LABOR COST COMPARISON REPORT IS NOW AVAILABLE

We are pleased to present the Werner International 2011 Labor

Cost Comparison, which is the only study comparing the hourly labor cost in over

40 countries worldwide. Our comparison covers all primary textile industry

sectors, consisting of spinning, weaving and dyeing & finishing.

As we did for previous editions, we would like to stress that the hourly labor

cost is one of the many factors impacting the competitiveness of the textile

industry. Nevertheless, it is the single most relevant driver in the continuous

process of global relocation of productions which has characterized our industry

in the last 30 years.

In an open global system less and less restricted (but heavily impacted) by

external factors such as exchange rates, important production flows will

continue to geographically reallocate in search of even temporary

competitiveness.

The previous labour cost comparison of 2008 took place during the global

economic and financial crisis of 2008/9, with the global economy being struck by

financial instability and questions of bank regulation and financial sector

oversight. Now in 2011/2012, the public debt crisis has taken centre-stage, with

discussion focusing on cutting public deficits, including the raising of taxes.

After the financial crisis, markets now question public finance sustainability

even in countries such as France. Within Europe, stabilizing and even reducing

labour costs is part of the overall economic mechanism to reduce the impact of

the debt crisis. In North Africa and the Middle East, the Arab Spring is having

a severe impact on the economic performance and industrial fabric of countries.

In addition, the impact of exchange rates between the various countries is, as

usual, playing an important role in comparing labour cost data between

countries. And although the exchange rate between the US$ and the € has been

fluctuating heavily over the last years, the exchange rate difference for most

European countries is below 4% between 2008 and 2011. However for countries like

Australia, Turkey, and a range of Asian and South American countries, the impact

of the exchange rate difference can be as high as 45%.

We all realize that a new business era is in front of us. An era for which

textile and clothing companies must prepare themselves with a strategic effort

in order to adapt, improve and redesign their business models to fight the

global impact of the financial and debt-crisis, with the aim of sustaining

growth and enhancing profitability.

To receive a full copy of the 2011 Labor Cost Comparison Report or to find out

how your company can participate in the 2012 edition, please e-mail us at

info@wernertex.com .

Back to top

SOURCING FROM CHINA AND SOUTH-EAST ASIA : THE WERNER VIEW

In 2012, imports of textiles & clothing into the USA remained stable, estimated

at around 100 bn US$ - or the same level as 2011. The year 2011 however saw an

increase of almost 9% compared to the year before. The picture is similar for

the European Union. Imports into the European Union in 2011 amounted to 93.1bn

€, almost 10% up from 2010, but forecasted imports in 2012 will be again at

around the same level as 2011, or slightly less. Imports into the main Western

consumer markets are stabilising again in 2012, similarly as in the financial

crisis year 2009. All other years in the last decade have shown considerable

growth of imports.

Does this mean that the era of cheap imports and, in particularly cheap China,

may be drawing to a close? Many observers quote that especially China's coastal

provinces are losing their power to attract cheap workers from the hinterland,

due to increasing labor costs, taxes and regulations

Taking a closer look at origins of imports, China represents a staggering 40%,

both of imports into the USA and Europe. It is true that China has lost slightly

percentagewise, but that is also true for other competing countries in 2012. In

absolute value terms, imports from China increased more than for example from

ASEAN countries, percentagewise on the large volume of imports originating from

China, this is of course less.

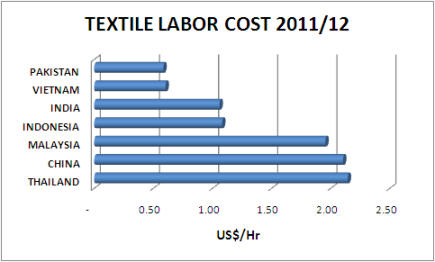

It is true that Chinese labor costs are increasing at a faster rate than ever

before. To demonstrate this, the table below is showing the latest labour cost

comparison for 2011/12, from the Werner International Labour Cost Comparison in

the Textile Industry.

But labor cost is just one element of competitiveness. The most critical factor

of competitiveness is labor productivity. However labor productivity is being

influenced by a wide range of variables such as level of technology, workplace

design and layout, factory size, material handling, training, product

complexity, ratio direct/indirect personnel, efficiency management, etc.

Compared to apparel companies in Cambodia and Vietnam, and because of the fast

increasing labor cost, Chinese apparel companies are now paying much more

attention to efficiencies in their production and supply chain, applying

innovative technologies and optimizing costs Other external factors, like

infrastructure, logistics and diversification for risk management still make

China a preferred hub for sourcing.

Over the last six years, Werner International apparel experts have been

executing more than 500 factory audits and surveys in China, Indonesia, Cambodia

and other South-East Asian countries. We have experienced that training at both

the operator and supervisor levels is often unsatisfactory. In addition to

operator training, on-the-job training for supervisors and managers is essential

to understand management techniques and manage and control their departments

better. Improvements in productivity of 15 to 20 percent are not exceptional,

often coupled with improved quality of a more complex product mix.

For more information, please contact

info@wernertex.com .

Back to top

SPECIALIZED MANUFACTURING SURVEYS

Werner International’s world class technical interventions are generally

conducted after the execution of a comprehensive manufacturing audit, which

covers (but not limited to) the following areas :

- machine and labor productivity

- quality performance

- raw material utilization

- level of technology

- human resources and skills

- process suitability

- working cycles

- delivery times

- material flows

- planning procedures

- costing

- information management

For over 75 years, we have provided this invaluable service as we believe

that such an in-depth survey of the existing production technology, product mix

and human resources will draw a clear picture of the overall performance which

can be obtained at departmental level as well as for your company as a whole.

Each assessment has the sole purpose to lay the foundation for further

successful development of the company.

The findings of each audit are then elaborated and consolidated into an

invaluable report which thoroughly shows your company’s current operational

performance in terms of strengths and weaknesses (as well as future threats),

identifying key performance gaps as well as improvement opportunities while

suggesting the necessary intervention methodology.

Contact our USA Office Director, Beth Govoni Marshall (bgovoni@wernerintl.com)

to receive a full proposal for a specialized Werner International manufacturing

audit.

POSTING JOB DESCRIPTION

A pioneer in the textile and apparel industries, Werner

International is unique among world leading consulting companies in being able

to combine specialized expertise in the technical areas with global marketing

and strategy know-how and networking. Our extensive team of highly qualified

textile and apparel manufacturing experts provides world class assistance to the

highest standard.

Werner International consultants are continually involved and updated in the

development of technology, equipment, automation and processing methods.

The Werner International network is currently seeking qualified individuals in

the following sectors:

- Weaving

- Spinning

- Dyeing and Finishing (with experience in JD F-22 Continuous Dyeing Process)

Please submit your CV directly to our USA Headquarters at

jobs@wernerintl.com

Back to top

|